Does Insurance Cover a Hit-and-Run?

By Pierce | Skrabanek

Published on:

February 13, 2026

Updated on:

April 21, 2026

.avif)

You're stopped at a red light. A vehicle slams into you hard enough to shove your car into the intersection. By the time you look up, the other driver has already swerved across two lanes and disappeared. You didn’t catch a plate number. You barely registered the make or model.

Your neck tightens. The trunk is crushed inward. Now you’re facing repair costs and medical bills without knowing who will pay for them.

Naturally, one question comes to mind: Will insurance cover a hit-and-run?

The answer depends on your policy, how quickly you report the crash, and whether the at-fault driver is ever identified. Here’s how insurance typically handles a hit-and-run accident.

Pierce Skrabanek helps hit-and-run victims pursue the compensation they're owed. Call (832) 690-7000 for a free case review.

When Does a Crash Qualify as a Hit-and-Run?

Texas law requires every driver involved in a collision to stop, exchange information, and render aid when someone is injured. Leaving the scene without doing so turns an ordinary accident into a criminal offense.

A hit-and-run doesn't require high speed or catastrophic damage. The classification applies when a driver:

- Rear-ends another vehicle and drives away before exchanging insurance details,

- Clips a parked car and leaves without providing contact information, or

- Strikes a pedestrian or cyclist and fails to stop and call for help.

Penalties escalate based on the severity of the crash. Leaving the scene of a collision involving injuries is a felony in Texas, carrying potential prison time and license suspension. Even property-damage-only hit-and-runs carry misdemeanor charges, fines, and points on the driver's record.

Understanding how the law defines a hit-and-run matters because that classification directly affects which insurance coverages apply and how your claim gets processed.

Does Auto Insurance Cover Hit-and-Run Losses?

Standard liability insurance only pays when you can identify the at-fault driver and file a claim against their policy. A hit-and-run removes that option entirely. The driver is unknown, and their insurer can't be billed for a claim that doesn't name them.

That leaves your own policy. Two types of coverage matter here:

Uninsured Motorist Coverage (UM/UIM)

This coverage pays for injuries and damages caused by a driver who has no insurance (uninsured) or whose insurance is not enough to cover your losses (underinsured) or cannot be identified, such as in a hit-and-run accident.

Texas doesn't require drivers to carry UM/UIM coverage, but insurers must offer it. Many drivers who declined it at the time of purchase may not realize they did. UM/UIM coverage helps pay for medical bills, lost wages, and pain and suffering up to your policy limits.

Collision Coverage

Collision coverage pays for the repair or replacement of your vehicle after a crash, regardless of who was at fault. It always requires you to pay your deductible first, and then insurance covers the rest. Without collision coverage, you pay for all vehicle damage from a hit-and-run yourself.

So, does your insurance cover hit-and-run losses automatically? Only when these specific coverages exist on your policy. Liability-only plans leave a gap that a hit-and-run exposes immediately.

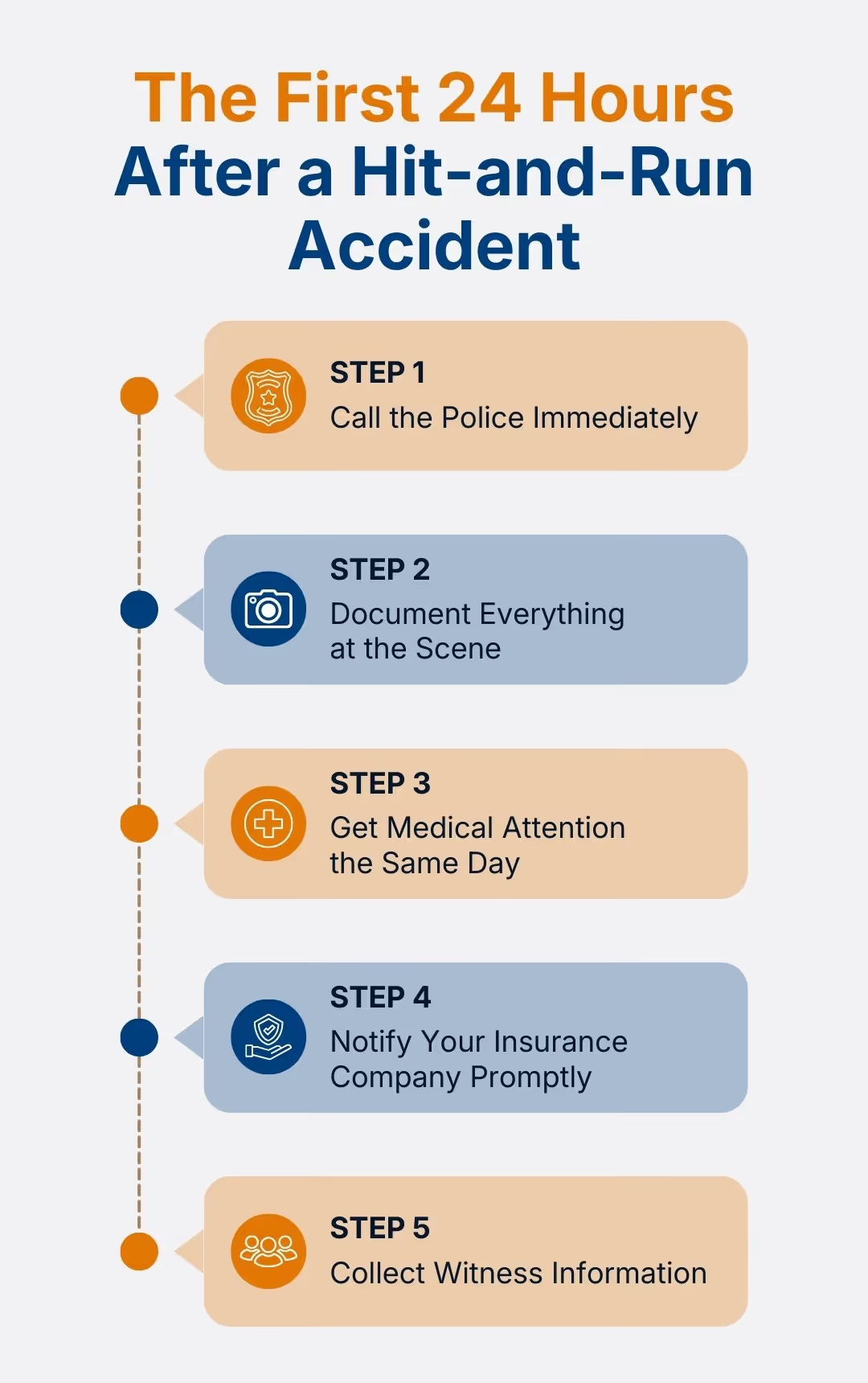

Filing a Hit-and-Run Insurance Claim

Building a strong hit-and-run insurance coverage claim starts with what you do in the first few hours after the collision. Thorough documentation connects the damage to the incident and gives your insurer less room to second-guess the details.

Call the Police Immediately

A police report creates an official record. Officers document the scene, collect witness statements, and log the locations of nearby surveillance cameras. Without that report, your insurer has far less to evaluate.

Document Everything at the Scene

Photograph your vehicle damage from multiple angles. Capture the road layout, traffic signals, debris, and skid marks. Write down the time, location, and every detail you can recall about the other vehicle, even partial ones.

Get Medical Attention the Same Day

Adrenaline hides injuries. Neck pain, headaches, and stiffness can surface hours later. A same-day medical visit ties those injuries directly to the crash and eliminates gaps your insurer could question.

Notify Your Insurance Company Promptly

Most policies require timely reporting after a car accident. Waiting weeks to file a claim gives your insurer grounds to challenge it or deny it outright. Provide the police report number, photos, and medical records when you call.

Collect Witness Information

Bystanders who saw the other car leave can provide vehicle descriptions, partial license plate numbers, or directions of travel. Their statements reinforce your account.

When Your Insurer Pushes Back

Having the right coverage on your policy doesn't mean the claims process will go smoothly. Hit-and-run claims are closely scrutinized because there's no secondary policy to split the cost. Every dollar paid comes from your plan.

Common pushback looks like:

- Questioning whether a hit-and-run actually occurred. Without a police report or witnesses, the insurer may argue that the damage happened in a different way. Single-vehicle damage on a busy road, for example, can be reframed as driver error.

- Disputing injury severity. A two-week gap between the crash and your first doctor visit gives adjusters leverage to argue your injuries weren't significant.

- Applying your deductible aggressively. Collision claims require a deductible before coverage kicks in. On lower-value claims, the deductible absorbs most of the payout, leaving little for the actual repair.

- Offering a fast, low settlement. Early offers reflect what the insurer wants to pay, not what the claim is worth. Accepting before understanding the full scope of your injuries locks in that number permanently.

Don't cover someone else's costs alone. For help recovering what you deserve after a hit-and-run accident, call Pierce Skrabanek at (832) 690-7000 or complete our online form for your free consultation. Act now to protect your rights.

What Happens When the Hit-and-Run Driver Is Found?

Police sometimes identify the driver through surveillance footage, witness tips, or paint transfer analysis. When that happens, the legal picture shifts.

Once identified, you can file a claim directly against their liability policy. Their insurance becomes the primary source of compensation for medical bills, vehicle repairs, and related losses. Your UM/UIM coverage then serves as backup when their limits fall short.

Criminal charges against the fleeing driver don't resolve your losses on their own. A conviction for leaving the scene doesn't pay hospital bills or cover months of missed work. A separate civil claim or insurance process handles recovery.

Does car insurance cover hit-and-run expenses even after the driver is caught? Yes. Collision and UM/UIM coverage still apply. Identifying the other driver opens an additional path forward.

What Compensation Can a Hit-and-Run Claim Recover?

The damages available after a hit-and-run are the same as in any car accident claim. Your coverage limits and the strength of your documentation determine how much you can pursue.

Recoverable losses typically include:

- Medical expenses. Emergency treatment, surgeries, imaging, physical therapy, and ongoing rehabilitation tied to crash injuries.

- Lost income. Wages missed during recovery, including reduced earning capacity when injuries prevent a return to full-time work.

- Vehicle repair or replacement. The cost to restore your car to pre-crash condition or its fair market value when the damage totals the vehicle.

- Pain and suffering. Physical pain, emotional distress, and the disruption to daily life caused by the crash and its consequences.

UM/UIM coverage handles injury-related damages up to your policy limits. Collision coverage addresses the vehicle itself. When the at-fault driver is eventually identified, a separate liability claim can pursue compensation beyond what your own policy provides.

Hit-and-Run Crashes Involving Pedestrians and Cyclists

Drivers aren't the only ones left dealing with a hit-and-run. Pedestrians and cyclists struck by fleeing drivers face the same coverage gap, often with far worse injuries.

A pedestrian hit in a crosswalk has no vehicle policy to fall back on. Recovery depends on:

- Whether they carry UM/UIM coverage through another auto policy in their household,

- Whether the driver is eventually identified, and

- Whether a personal injury claim can be pursued against the at-fault party.

Cyclists face a similar situation. Texas law treats bicycles as vehicles on the road, but most cyclists don't carry auto insurance. Medical bills from a serious hit-and-run accident stack up with no clear source of payment unless a household auto policy includes uninsured motorist protection.

So, does hit-and-run insurance cover these victims the same way? The coverage rules are identical, but access depends entirely on whether the injured person has the right policy in place. Many don't.

Protect Yourself Before a Hit-and-Run Happens

The time to review your coverage is before you need it. Look for these specific items on your auto policy:

- Uninsured/underinsured motorist coverage. Confirm it's active and note the limits. Texas insurers must offer it, but you may have waived it years ago without fully understanding what that meant.

- Collision coverage. Check your deductible amount. A $1,000 deductible on a $2,500 repair leaves very little reimbursement from a hit-and-run claim.

- Medical payments coverage (MedPay). This pays for your medical expenses after a crash regardless of fault. MedPay covers immediate costs, such as emergency room visits and imaging, while a larger claim is processed.

Adding or increasing these coverages before a hit-and-run puts you in a stronger position to recover when someone else drives away.

Do Hit-and-Run Claims Raise Your Insurance Rates?

Filing a claim after a hit-and-run shouldn't increase your premiums in most cases. Because you weren't at fault, the claim falls under your uninsured motorist or collision coverage rather than your liability policy. The question of does insurance cover a hit-and-run without penalizing the victim comes down to state law and your insurer's policies.

Texas law prohibits insurers from raising rates solely because a policyholder was involved in a not-at-fault accident. However, certain factors can complicate this:

- Multiple claims filed within a short period may trigger a rate review, regardless of fault.

- Collision claims count against your overall claims history, even when another driver caused the damage.

- Switching carriers after a hit-and-run claim can expose the filing during underwriting, potentially affecting your quoted rate.

Reviewing your policy's claims history provisions before filing helps you weigh the benefits of a claim against potential long-term costs.

Talk to Pierce Skrabanek After a Hit-and-Run Accident

A hit-and-run leaves you shouldering injuries and vehicle damage caused by someone who chose to flee the scene. Medical bills accumulate as recovery stretches on, and the person responsible for them is nowhere to be found.

Pierce Skrabanek has represented car accident victims across Texas for over 30 years, recovering more than $500 million in settlements and verdicts. Our bilingual attorneys and staff are ready to review your case and help you pursue the compensation you deserve.

Call (832) 690-7000 or contact us online today for a free consultation.

Pierce Skrabanek Fights for Results

We fight for the legal rights of clients nationwide in a broad range of areas, including maritime, industrial, and car or trucking accidents.

All Practice Areas

.avif)